- Newsroom

- Published on:

DACH region optimizes costs, while China builds the factory of the future

- New study: industrial companies increasingly using Industry 4.0 technologies internationally, with China and the U.S. extending their lead

- DACH region (Germany, Austria, Switzerland) showing a low propensity to invest and trailing when it comes to digital twin technology – which 84 percent of Chinese companies use in logistics

- Software-Defined Manufacturing (SDM) is becoming a key competitive factor: production excellence as a result of software, data, and IT/OT architecture

- Mexico and India included in the analysis for the first time: 61 percent of Indian companies surveyed already using AI in the production environment

Ludwigsburg / Munich – China is designing the factory of the future, while Europe, and the DACH region in particular, is struggling with the past. Established IT and OT landscapes as well as fragmented data structures are hampering progress here. Meanwhile, China is taking the lead in terms of supply chain transparency, digital twin technology, automation, and AI. India, Mexico, and the U.S. are also modernizing and implementing things faster than companies in the DACH region and the United Kingdom. These are the key findings from the Industry 4.0 Barometer 2026, which the management and IT consultancy MHP has published in collaboration with Prof Dr Johann Kranz from Ludwig Maximilians University (LMU) Munich.

Markus Wambach, Group COO at MHP: “Our data clearly shows that while China and the U.S. are consistently taking a software- and data-driven approach to transforming their production processes, the DACH region is not generating any momentum. Just three percent of companies in this part of the world are familiar with Software-Defined Manufacturing – in China and India the figure is 30 percent. Those who fail to strategically combine production control, data, and software risk losing their ability to compete.”

More than 1,200 people from industrial companies were surveyed for the Industry 4.0 Barometer 2026. Specifically, they were asked to assess the status quo with regard to Industry 4.0 in their own companies in the DACH region (Germany, Austria, Switzerland), the United Kingdom, the U.S., China and, for the first time, India and Mexico. The study highlights successes, but also reveals gaps in the subjects surveyed, including supply chain transparency, digital twin technology, Artificial Intelligence (AI), and Software-Defined Manufacturing (SDM).

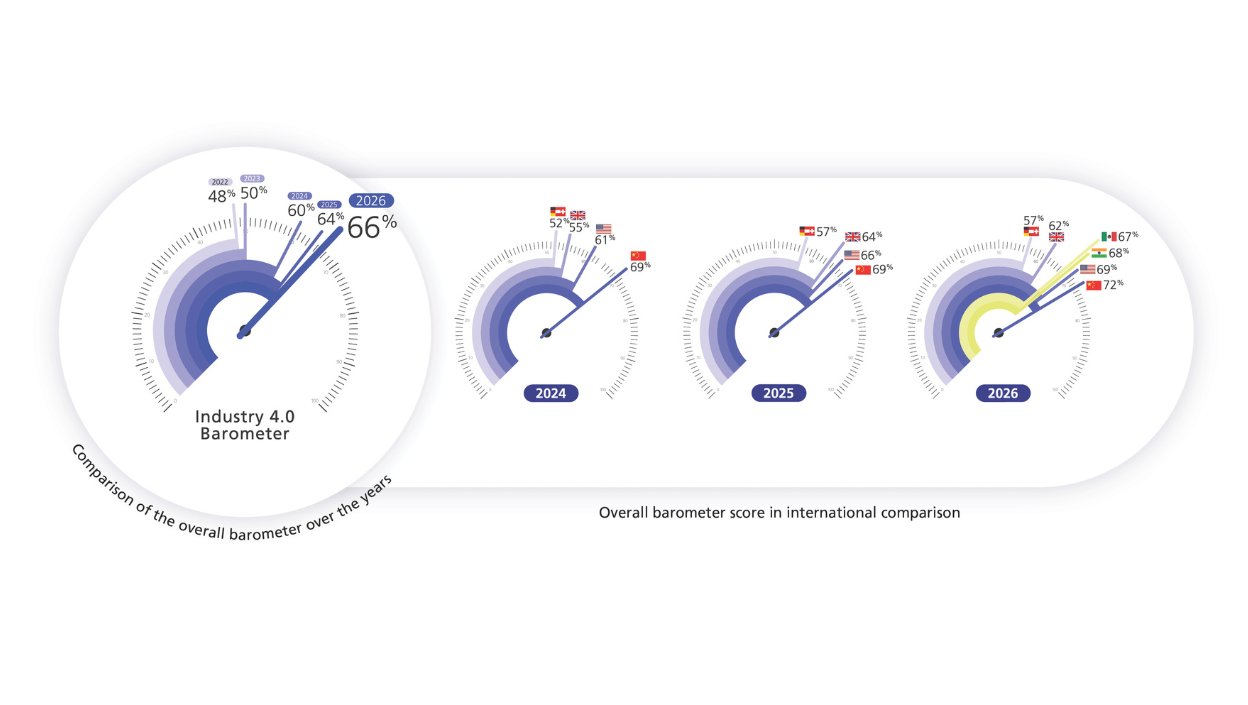

Degree of digitalization worldwide rises to 68 percent

Internationally, the degree of digitalization ascertained in industry continues to rise, with the overall barometer figure increasing from 48 percent (2022) to 68 percent today in all subject areas. However, two regions have fallen significantly behind: DACH is stagnating at 57 percent, while the United Kingdom has fallen to 62 percent (-2 percentage points compared to last year). Meanwhile, China achieved a figure of 72 percent (+3 percentage points), the U.S. 69 percent (+3 percentage points), India 68 percent, and Mexico 67 percent.

“The degree of digitalization in industry is increasing worldwide, with Europe also making progress,” said Dr Johann Kranz, Professor of Digital Services and Sustainability at LMU Munich. “In a comparison between countries, however, the U.S. and China are implementing digital production technologies faster and taking a more integrated and scalable approach than European companies. India and Mexico, which we were analyzing for the first time, are also showing better results in some cases.”

Causes of the faltering transformation

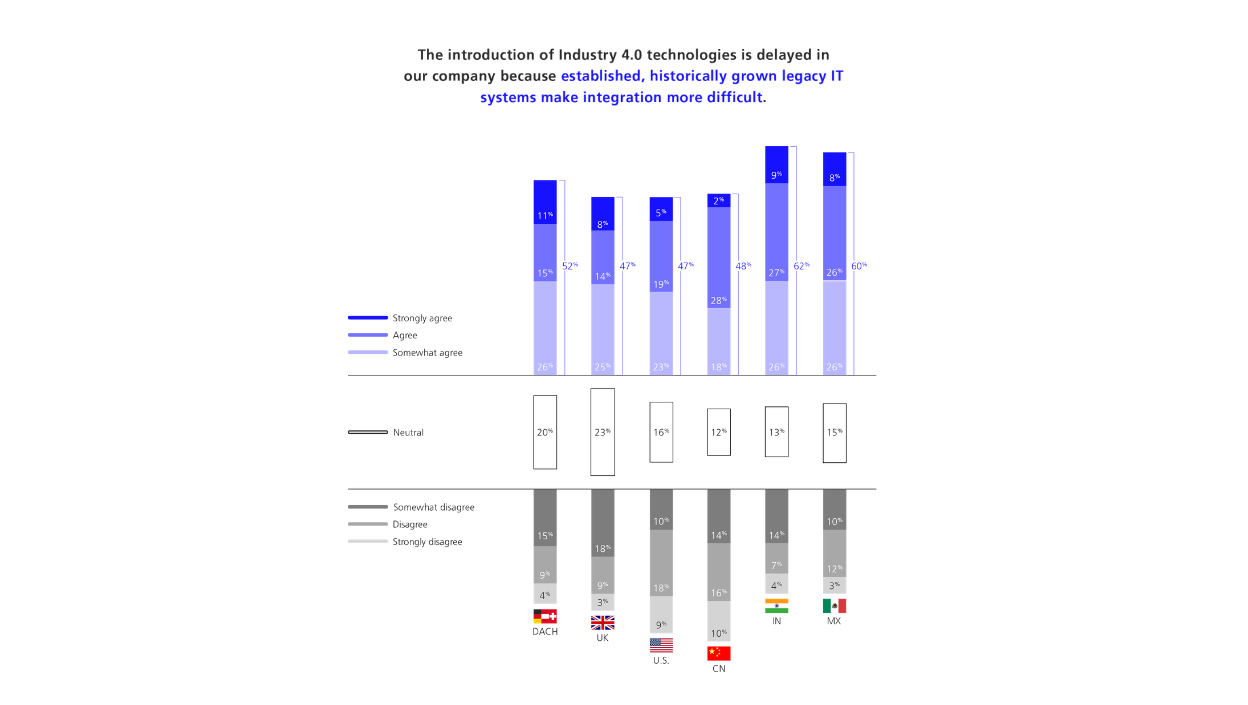

If the digital transformation is being hampered, it is usually due to technical reasons: heterogeneous legacy systems, fragmented data landscapes, and limited interoperability make it difficult to adopt new technologies. By way of example, 42 percent of the DACH companies surveyed see their data silos as an obstacle, while 52 percent consider their long-established IT systems to be a barrier. It is a similar picture at companies all over the world. Yet this year’s study reveals that these classic obstacles are overcome at different speeds, particularly in the areas of digital twin technology, Artificial Intelligence, and Software-Defined Manufacturing.

The digital twin is gaining ground faster than other technologies

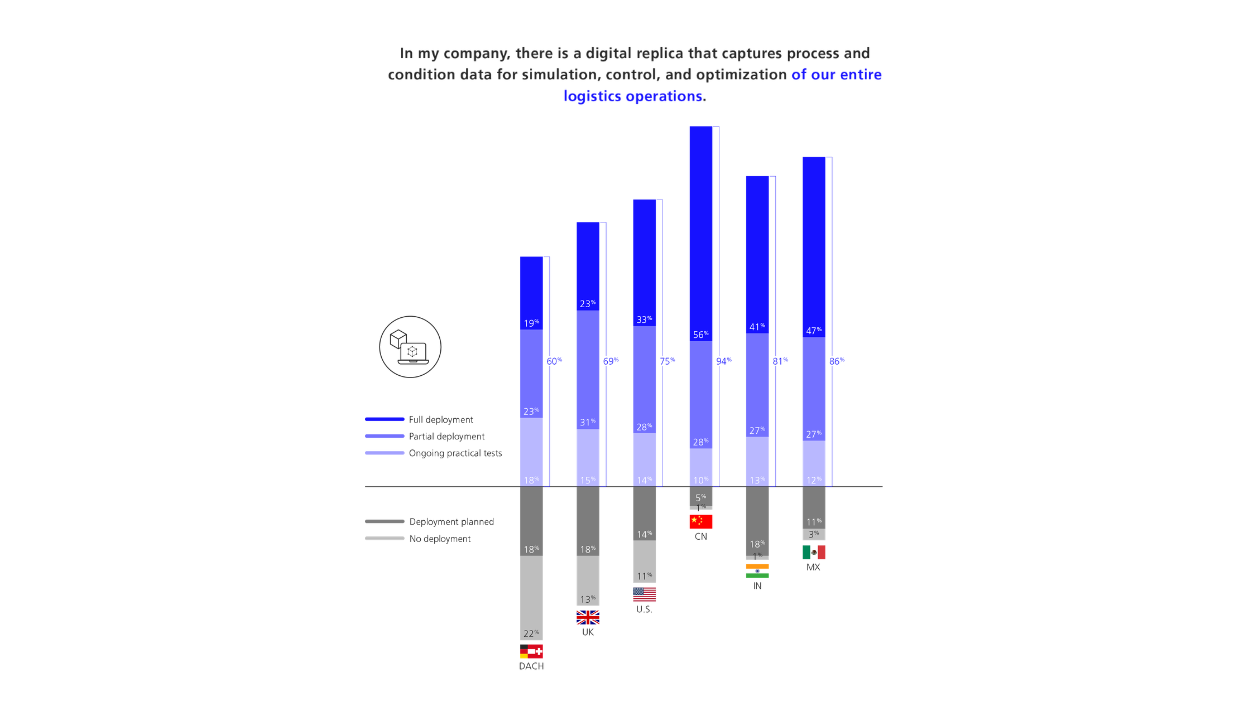

These differences are particularly striking in the case of digital twins. The barometer figure for their use in plants and machines has risen from 54 to 62 percent, while in logistics it has increased from 61 to 67 percent, representing the largest jump from the original figure of 30 percent (2022). This shows that the digital twin is taking off faster than any of the other technologies addressed in the survey.

Across all application fields, China is clearly in a leading position when it comes to the digital twin. This is especially evident in the context of logistics, where 84 percent of Chinese companies say they partly or fully use this technology. This is followed by Mexico (74 percent), India (68 percent), the U.S. (61 percent), and the United Kingdom (54 percent), with the DACH region lagging behind on 42 percent.

The DACH region is stuck in the AI hype gap

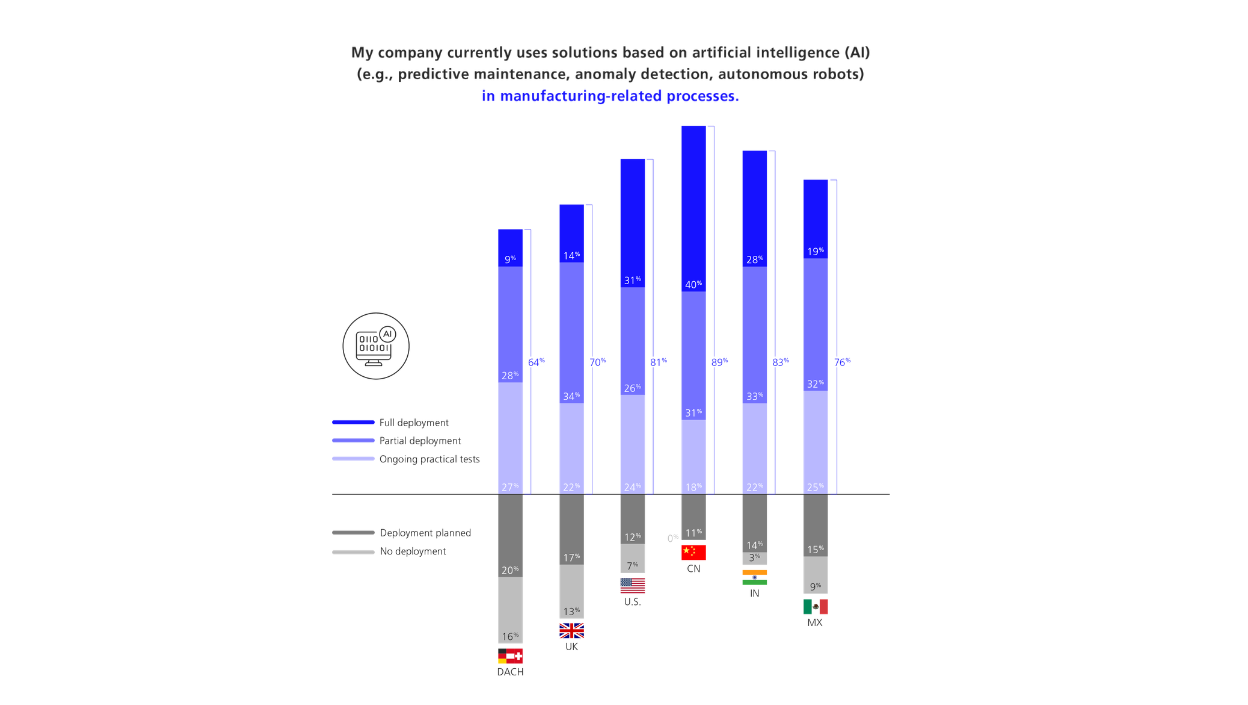

China and the U.S. also take a leading role in the use of Artificial Intelligence in production environments. When partly or fully using AI, Chinese players are out in front on 71 percent, followed by India on 61 percent, and the U.S. on 57 percent. Mexico (51 percent) and the United Kingdom (48 percent) are in the middle of the field, while the DACH region (Germany, Austria, Switzerland) is behind on 37 percent.

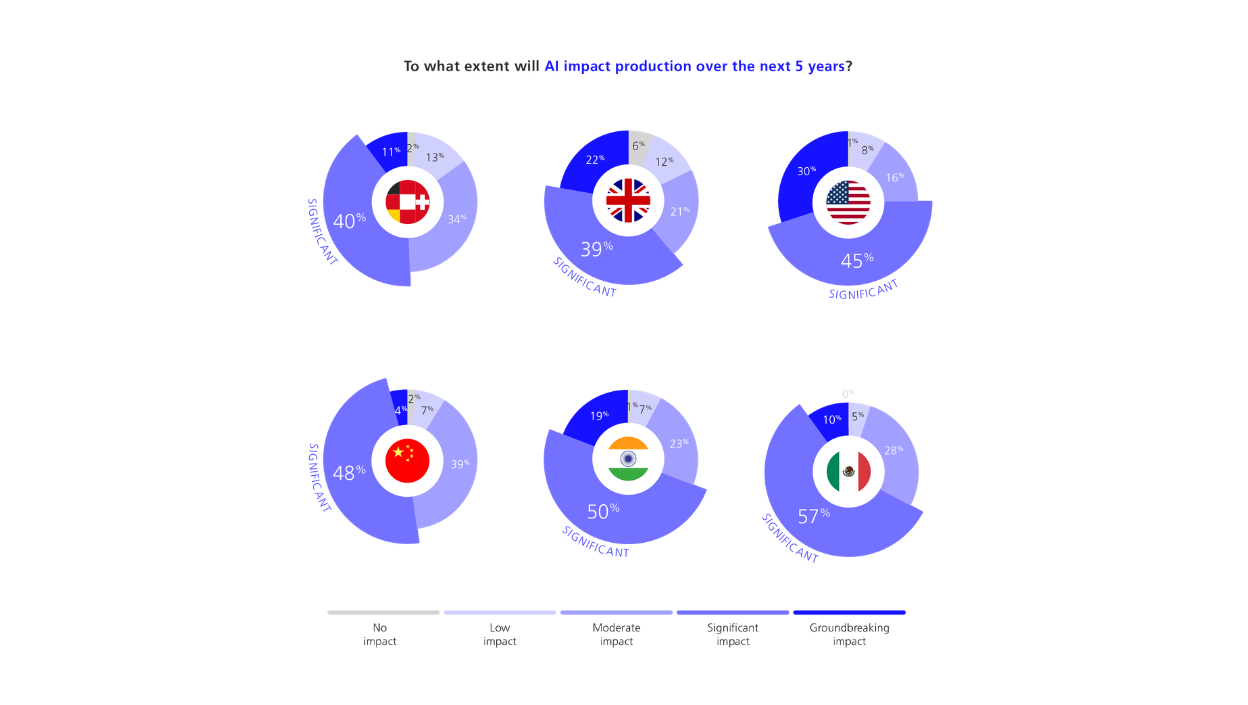

These findings reveal that many European companies are taking a rather cautious approach here. To date, they have only been using AI on a pilot basis, with a lack of deep integration into production processes. At the same time, the future impact of AI is rated highly. By way of example, 51 percent of companies in the DACH region expect it to have a “significant” or “groundbreaking” impact in the next five years. This gap highlights the fact that smart algorithms cannot be productive without solid foundations in terms of data infrastructures, sensor technology, and digital twins. Accordingly, AI remains a future promise in industrial practice but will not become an effective productivity factor (“AI hype gap”).

Software-Defined Manufacturing (SDM) is the new key skill

SDM separates production control from physical hardware and creates a central software layer that makes the manufacturing process flexible and scalable across different sites. CIOs play a key role here by becoming architects of the digital factory and taking responsibility for IT/OT integration, data literacy, and investment prioritization. Companies with a CIO state much more frequently that they are familiar with the SDM concept (+33.2 percent) and are more likely to integrate it into their overall strategy (+18.4 percent). There is also a greater propensity to invest (+13.8 percent), while the proportion of the budget earmarked for maintenance expenses is lower (-26.2 percent).

When comparing familiarity with the still nascent SDM concept, India and China are blazing a trail, with 30 percent of respondents in each of these countries attesting to a “very high” level of familiarity. The proportion is significantly lower in the DACH region (3 percent) and the United Kingdom (6 percent). The U.S. (14 percent) and Mexico (18 percent) are in the middle of the field.

Further upheavals are expected

The majority of respondents worldwide expect significant upheavals in the next ten years as a result of digitalization and software-driven approaches, with 31 percent holding the firm belief that their industry will undergo fundamental change and another 51 percent considering it likely. Once again, there are considerable regional differences in this assessment. In India, for example, 44 percent of respondents are convinced that software-driven approaches are altering their industry, while the figure in the DACH region is only 17 percent.

Digitalization requires a real willingness to invest: 71 percent of respondents in India state that their companies are willing to spend significant sums of money on new digital technologies. Mexico (65 percent) comes next, followed by the U.S. (59 percent). The figure is alarming for the DACH region, where just 29 percent are willing to invest.

“The DACH region (Germany, Austria, Switzerland) has a strong focus on efficiency and cost optimization, which means that strategic potential for growth, flexibility, and innovation often remains untapped,” explained Prof Christina S. Reich from FOM University of Applied Sciences, who is also a manager at MHP. “Emerging markets such as India, China, and Mexico, meanwhile, are pursuing more differentiated strategic goals. India, for example, is specifically focusing on improving quality due to its historical competitive position and global pressure. The aim here is to meet international standards and open up new markets.”

Overall, the findings highlight the fact that Europe is facing a huge modernization task. The main way for companies to maintain their competitive ability on the international stage lies in breaking down the technical barriers, standardizing IT/OT structures, and consistently gearing production toward software-based, scalable architectures. Software-Defined Manufacturing is becoming a yardstick for future industrial viability – and a critical success factor in the context of Industry 4.0.

About the Industry 4.0 Barometer 2026

The Industry 4.0 Barometer has been published since 2018 by the management and IT consultancy MHP in cooperation with Prof Dr Johann Kranz from Ludwig Maximilians University (LMU) Munich. The 2026 edition analyzes the statements of 1,206 people from industrial companies in the DACH region (Germany, Austria, Switzerland) (200), the United Kingdom (202), the U.S. (200), China (200) and, for the first time, India (200) and Mexico (204). The most strongly represented sectors are mechanical and plant engineering and information and communication technology, each with 13 percent, followed by the automotive industry (10 percent). The participants have roles across all hierarchical levels, most frequently working in IT (23 percent) and production (24 percent).

The questionnaire covers four areas – technology, IT integration, strategy, and goals – while equally examining barriers and drivers. There was also a focus on Software-Defined Manufacturing this time. Recommended courses of action round off the study for decision-makers, along with success stories from user companies and expert interviews.

The full study can be downloaded here.

You can request further information and ask about interview opportunities with MHP experts at any time.

The management and IT consultancy MHP has published the Industry 4.0 Barometer 2026 in collaboration with Prof Dr Johann Kranz from Ludwig Maximilians University (LMU) Munich. (photo: Adobe Stock)

Overall Barometer (photo: MHP)

AI impact (photo: MHP)

Distribution of AI solutions (photo: MHP)

Obstacles Industry 4.0 technologies (photo: MHP)

Distribution of the digital twin (photo: MHP)

Benjamin Brodbeck

Head of Public Relations and Press, Political & Government Affairs

Rebecca Vlassakidis

Spokesperson Digital Factory, Logistics & Customer Experience

Related News

MHP Newsroom

Need information about MHP or our services and expertise? We are happy to help and will gladly provide you with current information, background reports, and images.