- Blog, Digital Transformation

- Published on: 10.02.2022

- 4:34 mins

How sustainable are companies?

The EU taxonomy provides orientation

Can nuclear power and natural gas be sustainable?

The European Commission’s proposal to include these two energy sources in the EU Taxonomy has generated a lively debate, showing not only how controversial this topic is, but also that the Taxonomy Regulation is already in force.

So, what exactly is the EU Taxonomy? How does it define what can be considered sustainable and what are the consequences for businesses?

Objectives of the Taxonomy Regulation

The European Union’s Climate Law is a commitment to being carbon neutral in all sectors by 2050. This objective depends on a far-reaching transformation of the economy to move it toward carbon-neutral processes, energy production, and mobility. The EU expects these changes to require investment of at least one trillion euro this decade alone.

According to the EU Action Plan for Sustainable Finance, the funding will largely be provided by private investment from the real economy and financial sectors. However, to effectively steer investments toward sustainable economic activities, investors must first share a common understanding of which activities can be considered sustainable. This is where the EU Taxonomy comes in as a classification system with defined criteria.

When are economic activities considered environmentally sustainable?

To qualify as sustainable as defined by the Taxonomy Regulation, an activity must make a significant contribution to at least one of the six environmental objectives below, without significantly affecting the other environmental objectives:

The decision on whether the activity makes a significant contribution to a particular environmental objective is essentially based on Articles 10–16 of the Taxonomy Regulation. Delegated acts define additional“technical screening criteria” for certain industry-specific activities. The delegated acts function as a form of “green list” that defines a range of activities considered “green” under specific conditions. For example, the production of primary aluminum can be classed as making a significant contribution to climate protection if it can be done without exceeding specific limit values for emissions, carbon intensity, or power consumption. This activity can be classed as Taxonomy-aligned and environmentally sustainable if the production process also sticks to the “Do no significant harm” principle and upholds minimum social and human rights standards, such the United Nations Guiding Principles on Business and Human Rights.

The first delegated act that came into force on January 1, 2022 currently sets out the screening criteria for the “Climate Change Mitigation” and “Climate Change Adaptation” environmental objectives for activities from 15 different sectors. The Taxonomy Compass created by the EU provides an overview of the Taxonomy Regulation. In the future, this list will be supplemented with additional delegated acts that cover more activities and sectors.

Who is affected by the Taxonomy Regulation?

Who is affected by the Taxonomy Regulation?

The regulation particularly affects financial market participants such as investment funds, banks and insurance companies that are required to report under the Sustainable Finance Disclosure Regulation (SFDR) or provide financial products.

Approximately 11,500 real economy companies in the EU, which are required to submit a non-financial statement in accordance with the Non-Financial Reporting Directive (NFRD), must now also report the proportion of their expenditures that comply with the taxonomy. The EU Commission assumes that this "taxonomy alignment" will initially only be around 0 to 5 percent for many companies.

Disclosure based on the following indicators is mandatory:

- Proportion of sales revenue generated from products or services related to sustainable economic activities (turnover KPI).

- Proportion of capital expenditures related to assets or processes that are associated with sustainable economic activities (CapEx-KPI)

- Proportion of operating expenses related to assets or processes that are associated with sustainable economic activities (OpEx KPI).

The Corporate Sustainable Reporting Directive (CSRD), which is scheduled to come into force for the 2023 reporting year, is expected to extend the reporting obligation to smaller and medium-sized companies and will then affect around 50,000 companies in the EU. Companies that are not affected by the regulations can use the taxonomy voluntarily, for example to define and implement sustainability measures, to identify catch-up requirements and optimization potential, or to meet business partner requirements.

The EU taxonomy helps to create transparency about sustainable activities, channel investments and avoid greenwashing. It can also be assumed that environmental performance will become more of a focus for private and institutional investors in the future and will increasingly become a criterion for funding - as is already the case with the NextGenerationEU Fund. EU member states are also to define public measures, standards and labels for green financial products and corporate bonds on the basis of the taxonomy.

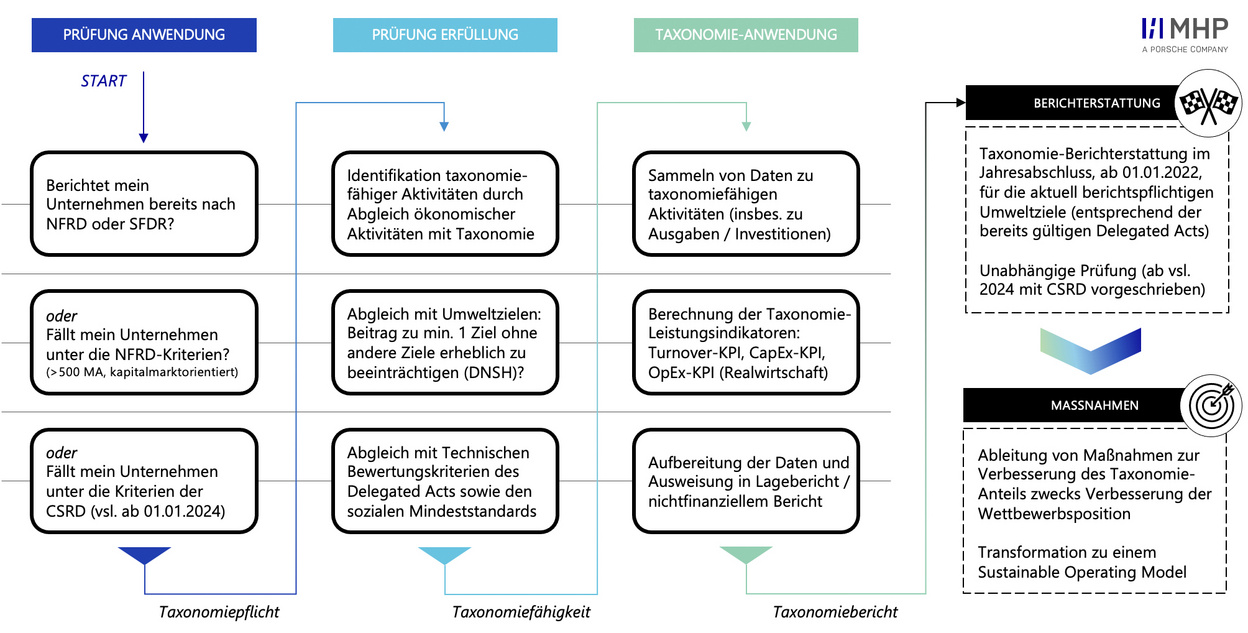

How is it checked whether activities are in line with the EU taxonomy?

A check of the taxonomy capability can be carried out using the scheme shown in the diagram. For this purpose, relevant activities must first be identified and assigned to the environmental goals of the taxonomy. The next step is to assess whether the activity makes a significant contribution to an objective without significantly compromising other environmental objectives, and whether minimum social safeguards are met in the process. The assessment should be based on a robust methodology and focus on greenhouse gas emissions for the first two environmental objectives. Then, the activity can be aligned with the technical assessment criteria of the Delegated Regulations. Based on these assessments, the required performance indicators are then calculated and integrated into the report.

The EU Taxonomy as another driver for sustainability

The combination of financial and non-financial indicators through the new EU Taxonomy is another clear signal that companies can already be analyzed from more than just a financial perspective. Transparency about the environmental and social impact of business activities is becoming increasingly relevant to policymakers, financial market participants, investors, and customers. And instruments like the EU Taxonomy are making these considerations a necessity. To successfully prepare for the stricter requirements and tightening framework conditions resulting from this transformation, companies must recognize that moving to sustainable business models is essential, both in terms of meeting expectations and not losing their license to operate. With this in mind, the question for companies is not whether the “green” transformation of the economy is possible, but how it will succeed. The EU Taxonomy is an initial regulatory requirement for companies of all sizes, and its relevance and importance will increase in the years ahead.

For this reason, we recommend analyzing the individual requirements of your business, pinpointing measures as early as possible, and using the regulatory requirements for transparency as a source of business potential. Please contact us if you are interested in discussing the impact of and implementation options for the Taxonomy Regulation at your company!